$FOUR Shift4 Q1 2025 Earnings Recap

Execution Amid Transition

FOUR 0.00%↑ printed a strong Q1. Volumes up 35%. Revenue ex-network fees up 40%. EBITDA margins at 46%. Free cash flow solid at $70.5M Core business is firing.

And markets reacted well — the stock jumped 12% after the earnings release. That followed a period of weak performance driven by tariff noise, recession fears, and headline attention on Jared Isaacman stepping back as CEO.

All real. But none of it reflects the reality of Shift4’s execution under the hood.

Let’s unpack the quarter and the setup going forward but first

📢 Jared’s Transition: Stepping Back, Not Out

Jared is preparing for a potential NASA mission. As part of that, he will:

Step down as CEO (Taylor Lauber takes over — already running ops)

Convert all his super-voting B and C shares into Class A

Relinquish control and reduce his voting power to match all shareholders

Still own ~25% of Class A and remain Chairman

This is good governance. It also removes a key overhang for institutional capital.

"Once the Senate votes on Jared’s NASA appointment, he will convert all of his B and C shares into Class A, relinquishing his super votes, and owning approximately 25% of the outstanding Class A shares." — Taylor Lauber

The playbook is staying the same — the hands executing it already were.

📊 Earnings Recap

Payment Volume: $45B (+35% YoY)

Gross Revenue: $848M

Gross Revenue Less Network Fees: $369M (+40% YoY)

Adjusted EBITDA: $169M (+38%)

Adj. EBITDA Margin: 46%

Free Cash Flow: $71M (42% conversion)

Adjusted EPS: $1.07

GAAP Net Income: $19.5M (–32% YoY)

Drop in GAAP earnings came from:

Interest expense tripling from $8M → $28.5M (post-M&A, rate-driven)

No repeat of $11M investment gains from Q1 2024

Margins are holding. Spread is stable. Cash flow is scaling.

🔁 Business Flywheel

Shift4's strategy is to:

Acquire vertical software with merchant relationships (POS, loyalty, gateway)

Bundle with Shift4’s payments

Cross-sell into the installed base

Scale margin, expand revenue per customer

It’s working.

Revel: 7,000+ locations already live on Shift4 payments

Givex: Loyalty/Gift stack embedded into Skytab, ~100 cross-sells already

Eigen: Gateway customers converting to full-stack payments

$20M+ in EBITDA synergies already realized in Q1

🌍 Global Expansion

Two years ago: 1 continent. Today: 6.

Europe: 1,000+ restaurants per month going live

LATAM: Enterprise wins onboarding

Vectron + Givex: Local distribution + software

Global Blue deal adds:

$500B+ luxury retail flow

Tax-free shopping + DCC bundling

Expected $80M revenue synergy by 2027

Still on track to close in Q3

Partners: Ant Financial + Tencent will remain on cap table post-close

💰 Capital Allocation

$63M in share repurchases in Q1

FCF positive and scaling

Debt from acquisitions covered by EBITDA + FCF ramp

~$1.1B in cash on hand

Management is disciplined. Leverage is manageable.

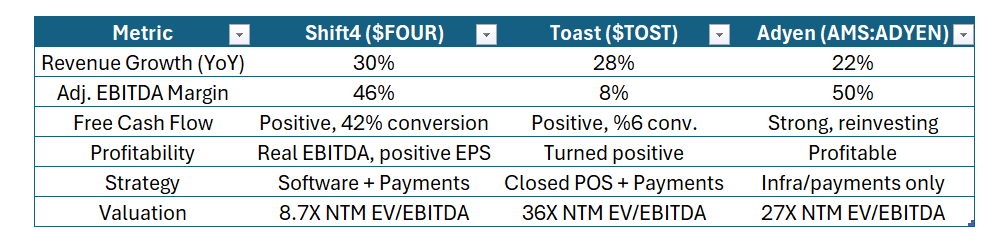

🆚 Peer Check: Toast vs Adyen vs Shift4

TOST 0.00%↑ is now profitable, though margins remain thin. Adyen is elite infra, but fully valued. FOUR 0.00%↑ is in the middle: profitable, scaling, and mispriced.

🔭 2025 Outlook

Raised full year guidance.

Revenue ex-network fees: $1.66–1.73B

Adjusted EBITDA: $840–865M

Volume stable: $200–$220B

🧠 Final Take

FOUR 0.00%↑ is executing.

Product and M&A strategy is producing real margin

Global expansion is working

Founder de-risks the structure, doesn’t abandon ship

Valuation still doesn’t reflect operating leverage

Ignore the headlines. Follow the fundamentals.

Follow

and subscribe for more high-conviction ideas.

What are your thoughts on the dilution because of acquisition. Hard for me to get a better read on valuation because of it